For example, if a strategy has an actuarial worth of 70%, then the insurance coverage business will pay about 70% of the total medical expenditures for everyone covered by that strategy. Together, you and everybody registered in the plan would pay the remaining 30% of the overall costs. This does not mean that you personally will pay 30% of your expenditures. Rather, this is an average throughout everyone registered in the plan. Your own costs will differ substantially from this quantity, depending upon how much care you utilize. While actuarial value doesn't inform you precisely what you will pay, comprehending it can help you pick which level of plan is ideal for your health needs.

Bronze plans will have low monthly premiums, however if you get ill or have an accident you will pay more in medical costs. Silver strategies are rather more financially protective and have an actuarial worth of about 70%. Gold and Platinum strategies have the greatest month-to-month payments but likewise are the most protective if you get sick or require a great deal of healthcare: they have actuarial values of about 80% and 90%, respectively. As soon as you pick which level of coverage is ideal for you, you can compare plans of a similar worth side-by-side. If your income is extremely minimal, you might get approved for a cost-sharing subsidy if you register for a silver strategy (these aids are described more above).

Typically silver plans have an actuarial worth of 70%, however with the cost-sharing aid, your silver strategies' actuarial value will vary from 73% to 94% (depending upon your earnings). This means you will likely pay less when you go to the medical professional or healthcare facility than you otherwise would with a silver plan. The Medical Insurance Marketplace Calculator approximates whether you might be eligible for expense gazing aids. If you are most likely eligible for an expense sharing subsidy, the calculator likewise shows what your silver plan's actuarial worth would be.

You can do a number of the exact same things on our site that you can do on the Market. You can shop, get costs and request medical and dental insurance both locations. The strategies you see on bcbsm. com are the very same plans you'll see on the Market. They have the very same advantages. https://www.benzinga.com/pressreleases/20/02/g15395369/franklin-tenn-based-wesley-financial-group-recognized-as-2020-best-places-to-work-in-u-s The rates are the very same, too. However not all our plans are readily available on the Marketplace, like our dental strategies that consist of adult vision. There are some other differences in between shopping on our website and the Market.

Welcome to the official Market information source for assisters and outreach partners. On this website, you'll discover information about assister programs and tools to assist existing and new Health Insurance Marketplace customers (What is gap insurance).

Get the answer to regularly asked concerns about Obamacare and the Health Insurance Marketplace. The federal Health Insurance Marketplace, which is likewise called the "Market" or "Exchange," is the site where individuals can search different health care plans offered under the Affordable Care Actcommonly known as "Obamacare" in addition to compare them, and purchase medical insurance. Some states, like California, provide their own Marketplace. If your state isn't using its own Marketplace, you can use the federal Market. The medical insurance plans are provided by private business, however are all needed to use all vital health advantages, such as hospital care, outpatient services, emergency situation services, maternity care, mental health and drug abuse treatment, prescription drug protection, laboratory services, and corrective services - What is commercial insurance.

Though, you might receive a Special Registration Duration if you have actually gone through a major life event like losing other protection, getting married, or having a child. A "exceptional tax credit" is a credit you can utilize to reduce your monthly insurance coverage payment when you register in a plan through the Market. Only specific people are qualified for lower premiums and lower out-of-pocket expenses for Market strategies. To receive lower premiums for a Market plan, your household earnings need to be between 100% of the federal poverty line and 400% of the federal poverty line. If you are used health coverage through your employer, you can buy a policy through the Health Care Marketplace, but you are eligible for subsidies just if your employer-provided insurance coverage isn't affordablethat is, if you have to contribute more than 9.

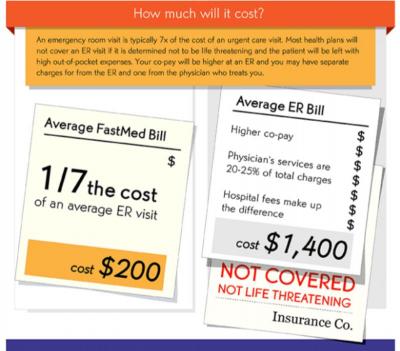

Top Guidelines Of What Is Comprehensive Car Insurance

If you do not get approved for your company's insurance coverage since you work part-time, you can get health coverage through the Market. There are four various categories of insurance coverage strategies offered through the Marketplace: Platinum, Gold, Silver, and Bronze. All of the classifications' strategies offer the same vital health benefits. The quality of care provided, or the access to doctors, does not differ in between strategy types. The various categories differ by the types and quantity of costs you'll pay. A Platinum strategy's premium is the highest, but you'll have lower out-of-pocket costs, like copays for visiting the physician Discover more here and for prescription drugs.

The Gold and Silver plans remain in between. A pre-existing condition won't keep you from getting health protection. Since January 1, 2014, no insurance provider can exclude you from protection because you have a chronic or disabling disease or injury because you have actually gotten current treatment for a medical condition. An insurer also can't charge you more if you have a preexisting condition. That said, if you presently have a private strategy that omits preexisting conditions, that strategy is "grandfathered" and does not have to change its rules. (A grandfathered specific health insurance coverage policy is a policy that you bought for yourself, or your family, on or prior to March 23, 2010 that hasn't been changed in certain specific methods that reduce benefits or increase costs to consumers.) If you can afford to buy health insurance coverage, but decide not to, you may need to pay a fee called the individual shared obligation payment (in some cases called the "private mandate").

The specific mandate is still in result for 2018, however is rescinded for 2019. (For more information, see What is the Obamacare Individual Charge in 2018?) Under Obamacare, preexisting conditions are covered, including pregnancy. Maternity care and giving birth are thought about necessary health advantages, which indicates all Marketplace health plans must cover themeven if you were pregnant before your protection starts. Some grandfathered specific health strategies, however, don't have to cover pregnancy and giving birth. (An individual health strategy is a strategy you buy yourself, not the kind you get through your job.) If you work part-time and can't get protection from your company, you can buy a strategy through the Marketplace (How to become an insurance agent).

However, if you can get health coverage from your employer, you can still purchase insurance coverage through the Market however you might not get approved for an exceptional tax credit and other cost savings based upon your income. If you lose your job-based coverage, you have the alternative of continuing your plan through COBRA for 18 months or of acquiring an individual plan through the Market. You do not need to wait up until an open registration period to sign up for a Marketplace plan if you lost your group insurance coverage. If you're self-employed, indicating you run your own service or do freelance or contract work, and you don't have workers, you can acquire a specific Market plan.